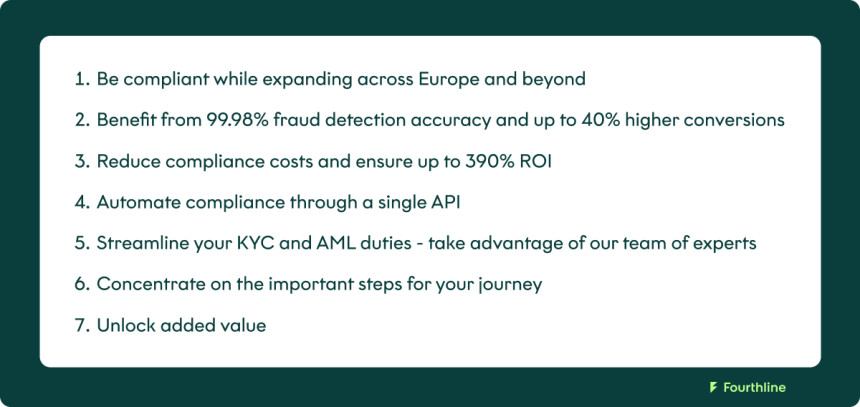

7 benefits fintechs can gain from Fourthline’s KYC and AML compliance solutions

The “Seneca effect” describes a process of gradual growth followed by a rapid decline. Just as it takes a balloon a couple of seconds to inflate but milliseconds to burst.

By The Fourthline Team

SHARE

The fintech industry knows the “Seneca effect” all too well. From cryptocurrency businesses to payment service providers and neobanks, there have been numerous examples over the past decade. After a period of steady growth, organizations have gone downhill or had to stop operating in certain jurisdictions. The number one reason? Regulatory failures.

However, oversight authorities in Europe don’t plan to loosen their controls. Just the opposite. After cases like Wirecard, the calls for stricter regulation are getting louder. Already, new frameworks are in the works or scheduled for enforcement in the short term. As such, fintechs must be prepared for greater regulatory scrutiny.

Fintechs compliance-related challenges: a quick overview

Fintechs are laser-focused on product development and growth. However, in their effort to offer incredibly innovative services and disrupt the market, they might miss prioritizing compliance early in their journey.

As a result, they can face costly business, regulatory, and reputational consequences, including:

-Failure to maximize conversions thereby increasing abandonment rates and eroding competitiveness

-Incurring significant higher compliance costs when facing tight deadlines from regulators

-Bearing expensive subscription costs due to working with multiple technology solution providers simultaneously or at different stages of their lifespan

-Failure to design effective risk controls resulting in increased regulatory scrutiny or lost revenue due to fraudulent account activity, which, in turn, increases reputational risk

-Sluggish expansion into new markets due to a lack of knowledge of local and regional regulatory standards

-Reduced organizational efficiency due to mundane compliance processes

-Throwing more people at the problem, causing organizational rigidity and complicating the process of achieving the vision of the company

-Failure to set up a secure environment to protect customer data storage and processing

7 benefits fintech organizations can expect from adopting Fourthline’s KYC and AML compliance solutions

Fintechs have redefined how consumers and businesses worldwide access, manage, invest or transact with their money. The industry has brought an experience with unmatched convenience, opening up financial services to millions of customers. However, this process has also helped to raise customer expectations, leading them to require seamless digital experiences. On top of that, the rapid growth and scale of the fintech industry has turned it into an attractive hotbed for financial criminals.

This begs the question - how can fintechs simultaneously ensure client satisfaction and protection? The answer lies in user-oriented compliance controls.

Regulatory compliance shouldn’t only be about following the rules. It should be about opening up opportunities for expansion, growth, and more satisfied clients.

Fourthline’s fintech partners are experiencing this first-hand. Over the past five years, we have been working with companies from all corners of the industry, including:

At Fourthline, we believe that fintech companies’ compliance needs are best served by someone who understands the niche inside out and speaks their language. As a result, we have built a fully modular solution that covers all steps required for KYC, AML, and GDPR-compliant client lifecycle - from initial identification and verification to continuous monitoring.

1. Be compliant while expanding across Europe and beyond

Regulators are increasingly looking towards the “same activity, same risk, same regulation”principle to lower the fintech industry’s barriers to entry and not hinder its ability to innovate. However, universal implementation will take time.

In the meantime, to manage threats to individuals, companies, and financial stability, regulators have introduced comprehensive EU-level directives, which different member-states can also back with locally-specific standards. Combining broader frameworks and targeted and pragmatic national regulations has accelerated the active cross-border and cross-sectoral cooperation.

However, it has also made international expansion tricky for fintechs. Penetrating new markets and onboarding and retaining new clients, while ensuring data protection and meeting the KYC and AML requirements, can become a complex and expensive process. This, in turn, can negatively impact the user experience.

But it shouldn’t.

Fourthline’s KYC and AML solutions help you remain compliant during onboarding and beyond, adhering to Union-level and local regulations in key markets such as:

-Austria

-France

-Germany

-Italy

-Netherlands

-UK

-Spain

-The rest of Europe & beyond

Before Fourthline, entering a new region was a long, drawn, tedious process taking anywhere between one to three months. Since implementing Fourthline, thanks to their existing reliance agreements and local expertise, we have added three new markets in less than two months with further launches already in the pipeline.

notes one COO and head of KYC at a fintech organization interviewed by Forrester for “The Total Economic Impact”, a commissioned study conducted by Forrester Consulting on behalf of Fourthline.

The case of Solaris also illustrates how an aspiring company, well-established in the German market, had to balance quick expansion across Europe with compliance excellence and first-class UX.

Fourthline's compliance expertise across different European jurisdictions has made rolling out into new markets far easier. Their deep domain knowledge allowed us to grow much faster than we otherwise could have.

explains Delia König, Managing Director of Identity at Solaris.

Similar is the case with N26, voted the best bank in the world in 2023. The digital bank has been onboarding clients through Fourthline for over five years and has been expanding across Europe. Today, it serves clients in more than 20 European markets.

2. Concentrate on the important steps for your journey

Fintechs come in all shapes and sizes. However, both early-stage startups and mature organizations share the same goal: Growth.

Compliance duties are often perceived as growth barriers. A common frustration of the respondents in the Fintechs Founders Survey is that regulators were still “all too unresponsive to the challenges faced by fast-growing tech companies.” Around 30% consider regulation a roadblock for further growth.

Fintech organizations have agility, innovation, convenience, and growth aspirations embedded in their DNA. As such, their focus should be on what they do best - driving change through their products and services. When it comes to compliance duties, they are best served by a flexible provider that will let them start small and respond to shifting priorities at every step of their journey - from onboarding the first to the millionth client.

Fourthline’s smart modular KYC and AML compliance solutions scale based on demand, adapting to each organization’s growth trajectory. As a result, fintechs can build compliant flows from day one and not need any other service provider at any point as they grow their business.

One COO at a fintech organization, interviewed by Forrester Consulting, states:

We grew at 1,500%, and Fourthline have been able to grow with us. They have proved that they are a very flexible and scalable partner for our operations.

Studying the experience of another prominent fintech that's partnering with Fourthline, Forrester notes:

Even when they went 10 times over the budgeted onboarding volume during a particular promotional event, Fourthline flexed up capacity on their end to meet the demand.

3. Automate compliance through a single API

Cutting-edge technology and operational agility are the bread and butter of fintechs. That is why they must collaborate with partners that are as innovative and forward-looking as they are.

In the context of compliance solutions, this translates to:

-Seamless integration, accelerating time to market

-Plug-and-play and drop-in solutions with minimal implementation efforts

-Modular compliance solutions enabling the design of partial or end-to-end compliant flows

-Flexibility to scale based on the organization’s individual needs

From document verification during client onboarding to re-KYC and continuous AML monitoring - these aren’t isolated interactions but elements of one journey. Make sure each step is worthy of your brand.

By integrating a single API, organizations can take advantage of Fourthline’s AI-powered solutions for KYC onboarding and advanced AML monitoring features and cover all bases with minimal effort.

According to Forrester’s report, organizations partnering with Fourthline have ensured massive productivity gains for their onboarding teams. For example, between 15 and 20 minutes have been saved per case, in 90% of cases, the entire verification procedure was completed in under five minutes.

Find out how we assisted NN in providing a secure and optimized digital onboarding solution for their new fully-fledged digital bank here.

4. Streamline your KYC and AML duties - takе advantage of our team of experts

Regulators are increasingly advocating for combining human expertise with the power of AI and automation during customer onboarding to prevent money laundering and terrorist financing.

Partnering with Fourthline means you will team up with industry experts working around the clock to identify evolving risk patterns and convert insight into forward-thinking prevention. Our specialists get ongoing training from leading institutions and authorities to ensure they are on top of their game. We are also actively collaborating with a diverse group of law enforcement authorities like Europol and the French police to crack down on money laundering in Europe. This allows us to keep up with the latest developments and provide you with valuable knowledge for financial crime prevention.

Whether you need to delegate a part or all of your compliance processes, our teams of anti-financial crime specialists based in Amsterdam and Barcelona are there to help.

Fourthline’s agile approach fits all organizational structures - from those seeking complete process automation, to companies pursuing lean operations with outsourced business processes, and fintechs with in-house anti-financial crime units that need additional assistance.

Partnering with us means you will get access to battle-tested technology, the latest know-how, and industry best practices that will keep you ahead of the curve. One head of business and KYC operations, interviewed by Forrester, shares:

Fourthline are good at keeping us informed about the changes and whatever new regulations are coming in for each country, which helps us respond to these changes much faster.

5. Benefit from 99.98% fraud detection accuracy and up to 40% higher conversions

Be it a payment processor, a digital bank, or a neobroker, all deal with user onboarding and transaction processing and have to balance satisfied clients with satisfied regulators.

In that sense, the design of a company’s client onboarding procedures can be critical to its existence and growth prospects. Once a point of differentiation, the speed of onboarding is now a customer expectation. Too loosen controls will expedite the process and increase conversion rates but expose you to higher risk. Meanwhile, overly-stringent onboarding procedures will ensure compliance but risk frustrating the clients you have fought to attract.

Fourthline’s robust AI-driven KYC processing combined with their regional regulatory expertise means we are able to onboard new customers faster while remaining fully compliant with local regulations.

— Head of KYC and AML at a fintech organization, interviewed by Forrester

The industry has long accepted the narrative that compliance is a cumbersome, expensive, inflexible, and slow process that increases friction. However, this is no longer the case. Thanks to technology and automation, fraud prevention and conversions are no longer mutually exclusive.

Fourthline’s compliance solutions, tested on millions of clients, ensure faster and smoother online account-opening experiences while collecting the information needed to meet local regulations and maintain security standards. As a result, organizations can ensure up to 40% higher conversions, 99.98% fraud prevention accuracy, and 75% lower false positives.

We used to convert roughly about 70% of new cases, which was higher than the industry average, but Fourthline managed to improve that by another 15%, which is truly impressive.

notes one Head of KYC and operations, interviewed by Forrester.

According to Forrester’s Total Economic Impact study, our solutions helped the interviewed financial service providers achieve a lower risk of fraudulent account openings than their existing internal systems or external vendors. This has unlocked $10.4 million worth of improved conversions, driving incremental account openingsand$2.7 million worth of reduced fraud exposure. One head of compliance and AML at a fintech shares:

Earlier, we were able to screen out less than 30% of fraudulent accounts, but with Fourthline, we have been able to improve that by at least 50%.

6. Reduce compliance costs and ensure up to 390% ROI

Unlike Tier 1 banks, fintechs often don’t have the resources to dedicate entire departments to managing compliance. Even those with sufficient VC backing must be cautious with their expenditures to maximize returns. Every euro saved can be a euro invested to accelerate growth.

Compliance is often a significant expense. The average annual compliance costs for some financial services firms can top 20 - 25% of the total cost of running the business. Furthermore, a 2022 study by Accenture found that 90% of respondents expect their compliance-related and compliance operating costs to increase by up to 30% over the next two years due to evolving business, regulatory, and customer demands.

Instead of being an unavoidable cash drain, with the right approach, organizations can turn compliance into a way to cut costs and maximize ROI. For example, Forrester’s TEI study found that Fourthline’s regtech solutions can generate massive gains for organizations, including:

-390% ROI

-Payback period of <6 months

-$13.3 million worth of improved organizational efficiency

Paired with unquantifiable benefits like minimal implementation efforts, lower abandonment rates, faster time-to-market, and reduced employee training costs, it can significantly optimize your organization’s compliance expenditures.

7. Unlock added value

Compared to Tier 1 banks, fintechs have a certain degree of freedom regarding compliance since they aren’t legally required to adhere to the most stringent requirements. However, many go beyond regulators’ demands to impose stricter fraud prevention controls.

Fourthline provides all the tools for those who want to be proactive and remain a step ahead of fraud.

For example, our insightful customer due diligence reports meet the auditing requirements of regulators across Europe and beyond. The fintechs interviewed by Forrester explained how Fourthline has helped them compile information quickly to facilitate the necessary cooperation with regulators during surprise audits, annual filings, and everyday work without disrupting their internal processes.

Furthermore, we are in continuous contact with European financial regulators and actively incorporate their feedback into our product stack to ensure you remain ahead in financial crime prevention.

On request of business partners audited by the Federal Financial Supervisory Authority and the Bundesbank, we have demonstrated our KYC flow and AML screening solution to explain in detail how they work. This unique situation shows how we can help our business partners and receive feedback from the regulator directly.

explains Michiel Visser, Product Owner at Fourthline.

Another added benefit is the opportunity to open new business avenues. Delia König, Managing Director of Identity at Solaris, says the partnership with Fourthline has equipped Solaris to assist the international expansion of the clients of its banking infrastructure. One example is Vivid Money. In its first year, the German challenger bank expanded into France, Spain, and Italy. The neobank plans to have a presence in all European countries.

We definitely want to work with Fourthline in all those markets,

notes Alexander Emeshev, Vivid Money’s Co-founder.

Last but not least, with Fourthline’s centralized secure identity vault, fintechs have one less thing to worry about. They can rest assured that their clients' data is stored and processed securely and in compliance with the GDPR.

Make compliance your competitive advantage

The business partners trusting Fourthline have opted for balancing compliance with operational agility and seamless experiences for their clients. As a result, they report higher conversions, reduced compliance costs, easier international expansion, and new business opportunities.

Experience it first-hand by making the first step - experience our regtech solutions with a free demo.